| United States Constitution | |

|---|---|

|

|

| The U.S. Constitution | |

| Preamble | |

| Articles of the Constitution | |

| I ‣ II ‣ III ‣ IV ‣ V ‣ VI ‣ VII | |

| Amendments to the Constitution | |

| Bill of Rights | |

| I ‣ II ‣ III ‣ IV ‣ V ‣ VI ‣ VII ‣ VIII ‣ IX ‣ X | |

| Additional Amendments | |

| XI ‣ XII ‣ XIII ‣ XIV ‣ XV ‣ XVI ‣ XVII ‣ XVIII ‣ XIX ‣ XX ‣ XXI ‣ XXII ‣ XXIII ‣ XXIV ‣ XXV ‣ XXVI ‣ XXVII | |

| View the Full Text | |

| Original Constitution | |

| Bill of Rights | |

| Additional Amendments |

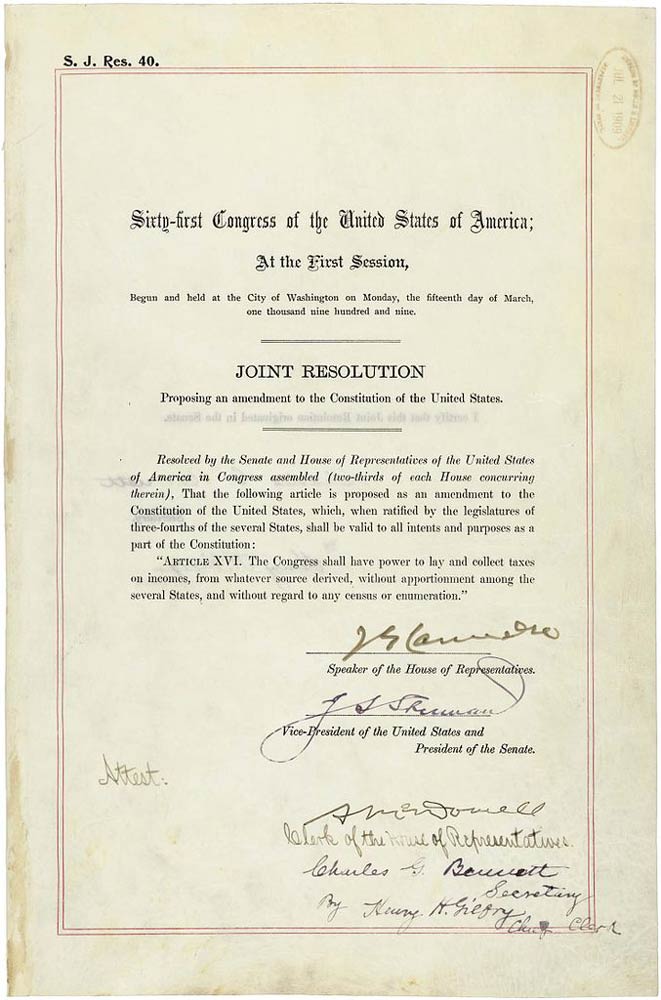

The 16th Amendment allows Congress to tariff an income tax without basing it on population or dividing it up among the states. The amendment is the constitutional law empowering the government to levy income taxes on Americans. Despite the fact that income taxes were implemented at different times in history, the laws were temporary and involved a national emergency. When the Sixteenth Amendment was adopted, the federal government was given more political power to set up the current form of taxation. This amendment was ratified on Feb 3, 1913.

Text

The Congress shall have power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

History behind the Amendment

In the U.S, the Treasury Department used to rely on sales taxes and tariffs for the majority of the federal budget. This continued to be the case until 1861, when President Abraham Lincoln instituted an income tax. With this, the initiative of taxes on wages gained reliability for funding portions of the government. At that time, President Lincoln needed more source of funds for the Civil War; therefore, Congress approved a progressive tax. The first income tax for individuals earning between $600 and 10,000 was 3%, while those who earned more than that garnered a greater percentage. This taxation ended in 1872.

The income tax was re-authorized by Congress in 1894, with a 4% tax on people earning more than $4,000. In the Pollock vs. Farmers’ Loan and Trust Co., Supreme Court Judges ruled that the income tax was not constitutional. In this case, the plaintiffs argued that taxing real-estate rental revenue was a direct tax and that the income tax should be removed. To avoid any other Supreme Court challenges, Congress proposed an amendment for income tax in the Constitution in 1909. The debate revolved around whether to have income tax or to impose tariffs on imports to collect subsidy for the Treasury. Democrats and Progressives proposed the initiative of taxing incomes while Conservatives disapproved this. Since the Conservatives knew that three quarters of the states would ratify the amendment, they approved the proposal to allow legislatures from the states to vote on the new amendment.

The income tax was re-authorized by Congress in 1894, with a 4% tax on people earning more than $4,000. In the Pollock vs. Farmers’ Loan and Trust Co., Supreme Court Judges ruled that the income tax was not constitutional. In this case, the plaintiffs argued that taxing real-estate rental revenue was a direct tax and that the income tax should be removed. To avoid any other Supreme Court challenges, Congress proposed an amendment for income tax in the Constitution in 1909. The debate revolved around whether to have income tax or to impose tariffs on imports to collect subsidy for the Treasury. Democrats and Progressives proposed the initiative of taxing incomes while Conservatives disapproved this. Since the Conservatives knew that three quarters of the states would ratify the amendment, they approved the proposal to allow legislatures from the states to vote on the new amendment.

On July 2, 1909, the 16th Amendment was authorized and then got ratification from the states on February 3, 1913. The income tax law became official on Feb 25, 1913 after the results of the ratification were certified by the Secretary of State. According to the Secretary of State and the U.S government Printing Office, the law got enough votes to ratify the Revenue Act 1913. This Act became the 16th Amendment. People making more than $500,000 in a year were taxed 7% of their income.

Effects of the Amendment

When the amendment became law in 1913, it clashed with a previous judicial decision in 1895 where the Supreme Court justices ruled that direct taxes were illegal. However, since the amendment was adopted, the case’s decision was effectively overturned.

Since the 16th Amendment was passed through the necessary steps before becoming a constitution law, the federal government was permitted to impose taxes on its citizens and people who earned wages. Since the adoption of the Sixteenth Amendment, the Bureau of Internal Revenue (BIR) was changed into Internal Revenue Service. The Internal Revenue Service was given power to enforce taxation law.

Conclusion

Up to date, there are still some debates on whether the 16th Amendment is constitutional or not. America’s Founding Fathers who designed the constitution wanted the power between the federal government and the states to be balanced. Therefore, the national government was not allowed to collect taxes from individuals directly. This means that the government could still collect revenue from the states in accordance to population, but it would leave the method of collection to the states. The federal government would use other methods which were less intrusive such as excise taxes, tariffs, and consumption taxes. This way the amount that the government could collect by its own authority was limited.

Most of the Founding Fathers did not like the idea of taxing individuals. In fact, the taxing of individuals was regarded as a last resort option and could only be implemented during war or other emergencies. It was not until during the Civil War that the first income tax was imposed, and it was repealed soon afterwards. When the Amendment was adopted in 1913, it only applied to 2 percent of the labor force, with the highest rate being 7%. This primed the way for the government’s unlimited access to revenue. This way, the government is able to fund important programs including education, law enforcement, and healthcare.